Thinking about applying for business credit cards for your non-profit organisation? There’s going to be paperwork, hoops to jump through and most likely an in-person branch visit required. We hope this article helps you understand what you can expect to go through when dealing with the bank, as well as offering some alternative options for obtaining cards for employee spending.

Non-profits are under more pressure than ever to ensure that all revenues and incomes are allocated wisely. If your charity is considering credit cards as an expense management method, here are some things to consider:

Do we want cards for our employees or cards for the business?

If it’s cards for the business itself, you’ll need to first open an account with the bank which will require an in-person visit and a lot of documentation.

If it’s cards for your employees, there’s a bit of back and forth to expect which we discuss below.

Are the employees that need cards based in head office? Or are they field workers or even volunteers?

Unless the employee has an existing personal account with the nominated bank, they are also expected to fill out a form, provide documentation on their financials, and visit a bank branch with 100 points of identification for verification

When do we want the cards?

The entire process for approved credit for either business banking or employees can be lengthy. You should expect it to take around 7 business days to have the card if the employee is already a member of the bank but around 21 business days if they are not.

How are you going to manage spend policy, receipt collection and new cards for employee departure?

Once you have your credit cards, how do we control what our employees use them on? How do we ensure the smoothest possible receipt collection to obtain employee buy-in? How do we replace the card if an employee leaves?

These questions will all require answers at some point so best to consider them now.

A step-by-step guide on getting credit cards for your charity

For NFPs who are ready to proceed with a credit card application, here’s an overview of what to expect:

Step One:

If the employee is not a current customer of the bank, they will need to fill out a three-page application form with their personal details (this cannot usually be done online as the bank needs to verify the individual with 100 points of identification in person).

Step Two:

They will need to take the application form with 100 points of identification to the closest branch. Then, once the bank has verified the individual;*

Step Three:

Take the form back to head office for a minimum of two signatures from Responsible Persons within your NFP to authorise the application. Generally, the role of a ‘Responsible Person’ is an important one for registered charities, as it would be its board or committee members, or trustees. See the ACNC website for more on this.

Step Four:

Submit the form to the bank for processing. You should be able to do this last step online, saving you another visit to the branch.

This process takes around 21 business days to receive the credit card, but it can be longer depending on risk assessment criteria. The bank may also ask for further information about the current financial situation.

Note:

If the employee is already a customer of the particular bank you’re applying for, the process should be easier. However, they will still need to fill out the application form with their personal details (this time, it can usually be done online). You will still need a minimum of two signatures from responsible persons.

Once the application is finished, the credit card will take about 7 business days to be sent out (again subject to approval).

At this point, we know what you’re thinking, “Well yeah, but if I want credit cards for my business, that’s just what you have to do”. That’s true. But did you know there are new alternatives to credit cards for businesses?

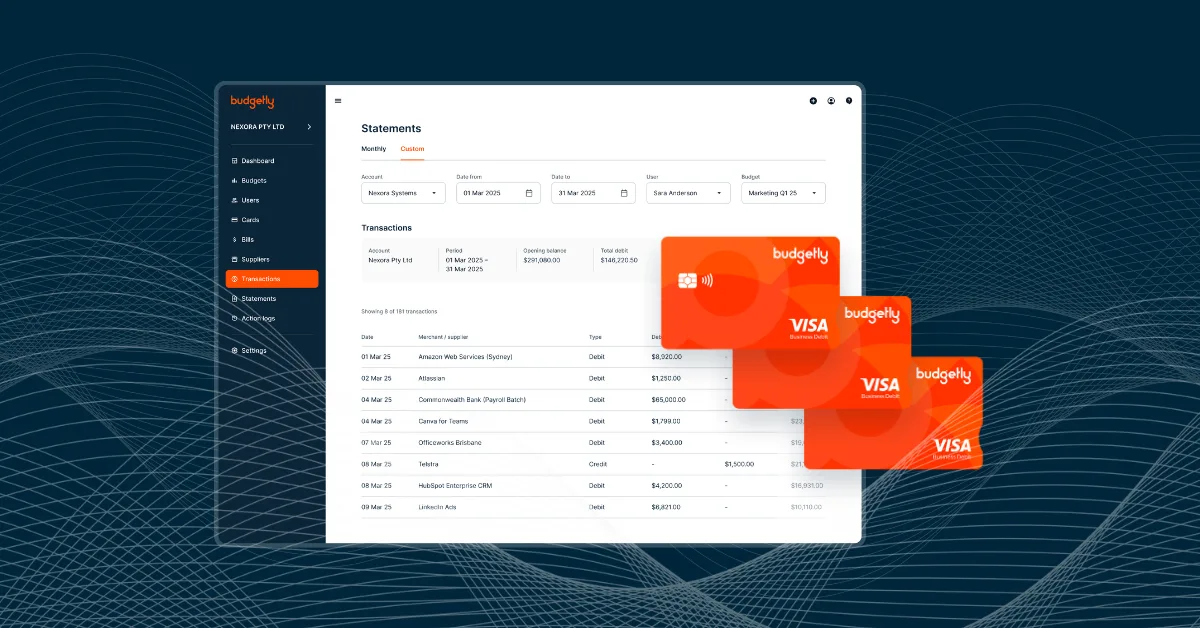

Have you heard of an “Expense Management Platform” that allows instant issuing of cards without dealing with the bank?

Well, it exists (albeit relatively new in Australia).

Expense management platforms are a popular alternative in the USA and in some European countries, and platforms with card issuing have finally made their way to Australia.

Here are some of the outcomes you’ll get from a business expense management platform:

- Instant card issuing. They use preloaded VISA smart cards instead of lines of credit which allow for instant issue. No more waiting weeks for a card to arrive.

- Total spend control. You can set rules in these platforms that ensure your employees can only spend what you want them to spend in the time frame you want them to. This means, you have a lot more control than a generic credit card limit.

- Instant visibility on all transactions across all cards in one spot. The software allows you to view all transactions (including receipts) as they happen for all cards. No more logging into different online banking portals.

- One-click receipt capture. Never have to chase receipts again with employees being able to click a button at the point of purchase to attach the receipt which then automatically flows into your accounting software along with the transaction information. This also ensures one-click receipt production during an audit.

If you’d like to talk to learn more about alternatives to the credit card system from the banks, talk to our experts today.

To learn more about Budgetly and our expense management platform, download our eBook, Managing Expenses with Budgetly. Alternatively, schedule a demo with us today to find out how we help businesses make expense management easier.

Disclaimer. Some NFPs do find that credit cards from the bank are the best solution for them. We speak to hundreds of NFPs who find the process extremely difficult. Our goal is to help you find the best budget management system for your needs.

*To ensure compliance, banks have their own processes around data collection, data verification, and risk assessment